Understand what happens after loan approval with a clear step-by-step guide, from signing documents to receiving funds and starting repayments.

Getting a loan is not just about applying and receiving the money.

For many people, the moment a loan gets approved feels like a big step. There’s often a sense that something important has been completed. After sharing documents, going through verification, and waiting for updates, reaching that stage can feel like crossing a checkpoint.

But here’s something that doesn’t get talked about enough— the real part begins after that.

A loan doesn’t end when it gets approved. In fact, that’s where your role becomes more active.

From that point onward, everything depends on how the loan is handled—how clearly the terms are understood, how payments are managed, and how consistent the repayment stays over time.

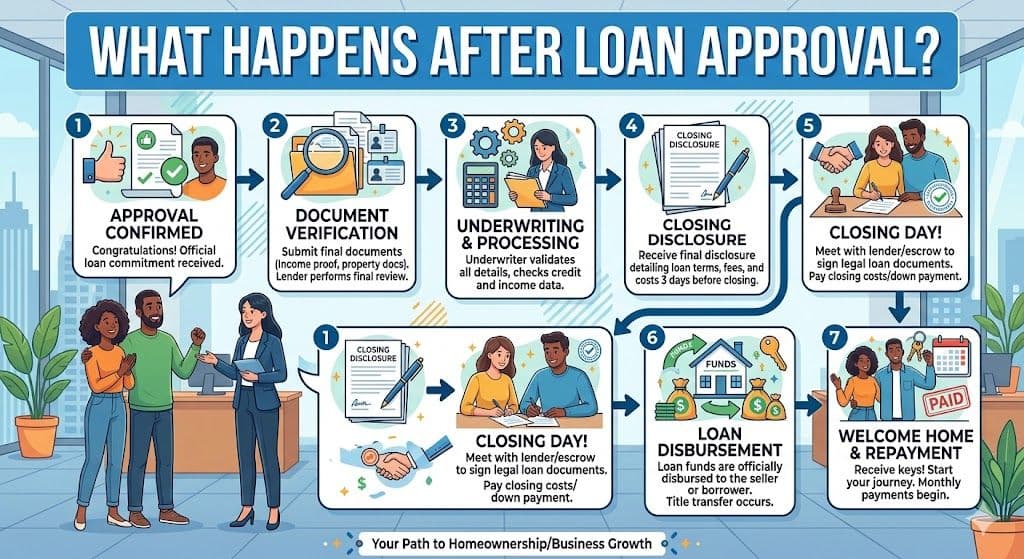

Let’s walk through what actually happens after a loan is approved, step by step.

What Banks or Lenders Do After Loan Approval

Once your loan is approved, the lender will move forward with the next set of actions.

The first thing you’ll receive is a confirmation. This could come through email, message, or direct communication depending on the lender.

In that confirmation, they usually include:

- The loan amount

- Repayment schedule

- Due dates

- Interest rate

- Any additional terms

This is not just a formality. It’s important to go through these details carefully.

After this, the lender proceeds with fund disbursement.

Depending on their process, the money may be:

- Transferred directly to your bank account

- Provided through other agreed methods

The timeline for receiving the funds can vary. Some lenders process it quickly, while others may take a few days.

At this stage, everything is structured. The repayment plan is already set, and the timeline has begun.

One important thing to remember here— not all lenders follow the exact same reporting system.

Many loans are reported to credit bureaus, which means your repayment activity can affect your credit record. At the same time, there are certain lenders that do not follow traditional credit reporting models.

For example, some lenders offering no credit check loans may not report to credit bureaus. This depends on the lender’s process and structure.

So it’s always worth knowing how your loan will be handled in that aspect.

What Lenders Expect After Giving the Loan

Once the funds are released, the lender’s expectation is simple.

They expect the repayment to happen as agreed. That’s it.

There are no complicated expectations beyond that. Everything is already defined in the loan terms:

- How much you will repay

- When you will repay

- How long the repayment will continue

From the lender’s side, the focus is on consistency.

They are not involved in how you use the money after disbursement. But they do expect that the repayment schedule will be followed without interruptions.

This is why it becomes important to stay aligned with the plan from the beginning.

What You Should Know After Loan Approval

This is where your responsibility becomes more active.

Once the loan is in your account, it’s important to stay aware of a few key points. These are simple things, but they make a big difference over time.

Repayment Planning

Before the first due date arrives, it helps to have a plan.

You don’t need anything complicated. Just make sure:

- Funds are available before the due date

- Payments are not left for the last moment

Some people prefer setting reminders. Others keep a fixed portion of their income aside for repayments.

The idea is to stay prepared rather than reacting at the last minute.

Repayment Amount

Knowing your repayment amount clearly is important.

This helps you organize your monthly or biweekly expenses accordingly.

Instead of adjusting everything at the last moment, it’s better to:

- Plan your spending after keeping the repayment amount aside

- Treat it as a fixed commitment

This keeps things more predictable.

Repayment Date

Missing a due date can create unnecessary complications.

That’s why it’s useful to:

- Set reminders on your phone

- Mark the date in your calendar

- Keep alerts a few days in advance

Even a small delay can lead to additional charges depending on the lender.

And in many cases, delayed payments are also reported to credit bureaus, which can affect your credit record.

So keeping track of dates is one of the simplest ways to stay on track.

Interest Rate

Your interest rate plays a role in how your total repayment is structured.

Understanding this helps you decide:

- Whether to continue as planned

- Or repay earlier if you have extra funds

Some borrowers choose to close their loan early when they have surplus money. This can reduce the total interest paid.

But before doing that, one thing to check is— does your loan have a prepayment charge?

If there is no additional cost, early repayment can be a useful option in certain situations.

Delayed Payment Charges

If a payment is missed or delayed, lenders may apply a penalty.

This can:

- Increase the total repayment amount

- Affect your repayment record

Over time, repeated delays can also reflect in your credit history if the lender reports to credit bureaus.

This is why even a simple step like setting reminders can prevent unnecessary complications.

A Small Practical Example

Let’s make this easier to understand with a simple situation.

Imagine someone takes a personal loan with a fixed repayment schedule.

If they:

- Note down the due dates

- Keep the repayment amount ready

- Follow the schedule consistently

The loan stays smooth from start to finish.

On the other hand, if they:

- Forget due dates

- Delay payments frequently

- Don’t track the balance

The same loan can become difficult to manage.

So the difference is not in the loan itself—but in how it is handled after approval.

Common Things People Overlook

Even though loan terms are clearly provided, some details are often missed.

For example:

- Not reading the full repayment schedule

- Ignoring prepayment terms

- Forgetting due dates after the first few payments

These are small things, but they can affect the overall experience.

Taking a few minutes to review everything at the beginning can make the process smoother.

FAQ Section

What happens immediately after a loan is approved?

After a loan is approved, the lender shares the loan details, including repayment schedule and terms. Then the funds are released to your account based on their process.

When does repayment start after loan approval?

Repayment usually starts as per the schedule provided by the lender. This could be within a few weeks or based on the agreed timeline.

Can I repay my loan earlier than the schedule?

In many cases, yes. But it depends on whether the lender allows early repayment without additional charges. Always check the terms before making an early payment.

“What is the most important thing to do right after receiving a loan amount?”

The most important step is to understand the repayment structure clearly. Note the due dates, keep track of the repayment amount, and plan your expenses around it. When everything is clear from the beginning, it becomes easier to follow the schedule without confusion.

Final Takeaway

A loan does not end at the time of approval.

That moment is just the starting point.

What really matters is how the loan is managed after that—how consistently payments are made, how well the schedule is followed, and how clearly everything is planned from the beginning.

When handled properly, a loan remains structured from start to finish.

So before applying, it’s good to understand the process. And after receiving the loan, it’s even more important to stay consistent with the repayment.

That’s what completes the full cycle of borrowing— not just receiving the money, but closing it responsibly.