Need a loan in SLC but your credit's rough? Here's how no-credit-check loans work in Utah, what they cost, and how to borrow without digging a deeper hole.

It's 6:45 on a Tuesday morning, and you're about to leave for work when your car makes a noise that sounds expensive. The mechanic in Murray says it's the transmission — $1,400 to fix. You've got maybe $300 in checking. Your credit card's maxed. And the last time you applied at your bank on State Street, the loan officer gave you that look. The one that says your 510 credit score already answered the question for her.

So you start Googling. "No credit check loans Salt Lake City." And you find a dozen options — but which ones are actually safe? Which ones won't leave you worse off than a broken transmission?

That's what this guide is for. Not a sales pitch. Just a clear look at how no-credit-check loans work here in the Salt Lake Valley, what Utah law says about your rights as a borrower, and how to use one of these loans without falling into a cycle you can't climb out of.

What No Credit Check Loans Actually Are (and Aren't)

Here's the deal. When you walk into a traditional bank — Zions, Mountain America, whoever — they pull your credit report. That three-digit number decides whether you get a yes or a no. For a lot of Salt Lake City residents, that number hasn't been kind. Maybe you went through a divorce. Maybe medical bills from a trip to the U of U ER tanked your score. Maybe you just never built credit in the first place.

No-credit-check loans skip that step. Instead of looking backward at your credit history, lenders look at what's happening right now:

Your current income. Are you working? Can you prove it with pay stubs or bank statements?

Your bank account. Is it active? Not overdrawn every week?

Your residency. Do you actually live in the Salt Lake area? Lenders want to know you're local.

Because the lender is taking on more risk — they don't have your credit report as a safety net — interest rates are higher than what you'd get at a credit union. That's the tradeoff. And it's an important one to understand before you sign anything.

These loans are built for short-term gaps. The car that broke down. The furnace that quit in January. The medical bill that showed up two months after the ER visit. They're not meant for long-term financing or recurring monthly expenses.

What Salt Lake City Residents Are Actually Paying in 2026

Let's talk real numbers, because context matters.

Rent in the Salt Lake Valley is averaging about $1,900 a month for a standard apartment. If you're commuting from Sandy or Draper, you're spending $200-plus a month on gas and vehicle maintenance. Groceries for a family of four? You're looking at $800 to $1,000 a month. Daycare — don't even get me started.

Point is, most people aren't sitting on a pile of savings. When something unexpected hits — and it always does, eventually — there's no buffer. That $1,400 transmission repair might as well be $14,000 if you can't get to work without your car.

That's where a short-term loan makes sense. Not because it's cheap. Because the alternative — losing your job, falling behind on rent, or borrowing from a source with even worse terms — costs more.

Utah Law Has Your Back (More Than You Think)

Utah gets a reputation for loose lending regulation, and honestly, some of that's earned. There's no interest rate cap in the state. But the rules that do exist? They're actually pretty solid protections for borrowers. Most people just don't know about them.

Here's what changed under the updated Utah Deferred Deposit Lending Act — including updates that kicked in with SB0329:

The 10-Week Rollover Limit. A payday loan can't be rolled over more than 10 consecutive weeks. After that, interest stops accruing on the principal. This is huge — it puts a ceiling on how much a single loan can cost you.

Right to Change Your Mind. Took out a loan and immediately regretted it? You've got until 5:00 PM the next business day to return the money and walk away without paying a dime in fees.

Income Verification Required. Lenders can't just hand you money — they have to verify your income or pull a consumer report to make sure you can realistically pay it back. This protects you from borrowing more than you can handle.

Partial Payments Always Accepted. Got an extra $50? You can throw it at the principal anytime, and the lender has to accept it. No extra charges, no minimum threshold beyond $5.

Knowing these rules changes the game. You're not walking into a lender's office blind — you're walking in with leverage.

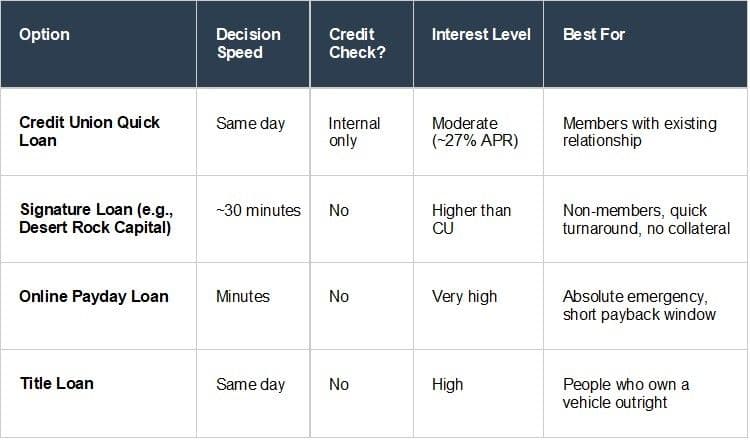

Comparing Your Options in the Salt Lake Valley

Not all no-credit-check loans are the same. Here's how the main options stack up for SLC residents:

Quick note on credit unions: several Salt Lake County credit unions — including a few along the Wasatch Front — offer "Quick Cash" products that skip the traditional credit check. If you're already a member, that's worth a phone call before you explore other options. Rates tend to be lower.

But here's the catch — you usually need to already be a member, and some have waiting periods. If you need money today and you're not a member anywhere, that option closes fast.

How to Borrow Smart (Not Just Borrow)

Getting the loan isn't the hard part. Using it wisely is. And that's where a lot of people in the valley get tripped up — not because they're careless, but because nobody walked them through a plan.

Borrow the exact amount you need. Your car repair is $1,400? Borrow $1,400. Not $2,000 "just in case." Every dollar over what you need costs you interest. That extra $600 of cushion might end up costing you $150 in fees you didn't need to pay.

Set a payoff target before you sign. Look at your next two or three paychecks. Can you pay this back in 30 days? 60? Pick a realistic timeline and work backward. If a lender offers biweekly payments, match those to your pay schedule.

Only work with licensed Utah lenders. Check the Utah Department of Financial Institutions website. If a lender isn't listed there, walk away. Full stop. Licensed lenders have to follow the consumer protections we just talked about. Unlicensed ones don't.

Read the total finance charge — not just the monthly payment. The monthly payment might look manageable, but what does the loan cost in total? That's the number that matters. A $1,000 loan that costs you $1,380 total is a very different deal than one that costs you $1,180.

What a No-Credit-Check Loan Actually Looks Like — Real Numbers

Let's walk through a real scenario, because vague advice doesn't help anyone.

Say you need $1,000 for an emergency car repair. You walk into a local lender in the Salt Lake area. They don't run your credit. They verify your income — you bring in two recent pay stubs showing you make $2,800 a month.

You're approved for $1,000. The repayment plan: 24 biweekly payments. That works out to roughly $65 per payment. Over the life of the loan, you'll pay back around $1,560 total — meaning the cost of borrowing is about $560.

Is that cheap? No. But compare it to the alternative. If you can't get to work, you lose shifts. At $18 an hour, missing five shifts is $720 in lost income. The math isn't complicated — borrowing $1,000 to keep your income flowing is the less expensive option, as long as you pay it back on schedule.

And here's the part most people don't realize: if you pay it off faster, you save on interest. If you can knock out that $1,000 in the first three months instead of twelve, you might cut that $560 in interest charges nearly in half. No prepayment penalties — your extra payments just reduce what you owe.

What One SLC Borrower Learned the Hard Way

A loan officer at Desert Rock Capital's Salt Lake City location shared this story (details changed for privacy):

A woman came in last winter needing $800 for a broken furnace. Utah winters don't wait around for your savings account to catch up. She'd been turned down at her bank because of a medical collections account from three years earlier — a bill she didn't even know had gone to collections.

She borrowed the $800, set up biweekly payments matched to her pay schedule, and paid the whole thing off in four months. Total cost of borrowing: about $290. She told the loan officer later that the hardest part wasn't paying it back — it was getting over the embarrassment of asking in the first place.

That's something we hear a lot. There's a stigma around these loans that doesn't match reality. People aren't irresponsible for needing help with a $800 furnace. They're just dealing with life in a state where the average household doesn't have $1,000 in emergency savings.

About Desert Rock Capital

Desert Rock Capital offers signature loans from $100 to $3,000 — no credit check, no collateral required. Repayment is structured as biweekly installments (up to 36 biweeks), so there's no lump-sum surprise at the end. No balloon payments, no prepayment penalties if you want to pay it off early. The SLC branch is open until 8 PM for people who can't get there during normal business hours.

It's not the cheapest option in the world — no-credit-check loans never are. But it's transparent, it's fast (most people get a decision within 30 minutes), and it's built for the kind of short-term situation we've been talking about.

Frequently Asked Questions

How much can I borrow without a credit check in Salt Lake City?

Utah allows installment loans up to $3,000. How much you're actually offered depends on your verified income and the lender's internal criteria. Most first-time borrowers qualify for somewhere between $500 and $1,500.

Are no-credit-check loans legal in Utah?

Yes. They're legal and regulated by the state under the Utah Deferred Deposit Lending Act. Utah doesn't cap interest rates, but it does regulate rollovers, require fee disclosure, and mandate income verification. Always confirm your lender is licensed through the Utah Department of Financial Institutions.

What happens if I can't make a payment?

Under Utah law, a lender must give you 30 days' notice before taking any civil action. Most lenders will work with you on a payment plan if you reach out early. The worst thing you can do is go silent — contact your lender the moment you think a payment will be late.

Can I pay off my loan early without a penalty?

With most Utah installment lenders that offer signature loans, yes. There's no prepayment penalty. Any extra payment goes directly toward your principal balance, which reduces the total interest you'll pay.

What's the difference between a payday loan and a signature loan?

A payday loan typically has to be repaid in full on your next payday — usually within two weeks. A signature loan spreads repayment over multiple installments, which is easier to manage on a tight budget. For a deeper comparison, check out our guide on installment loans in Utah.

Your Next Step

If you're sitting in the same spot as that woman with the broken furnace — staring at a bill you didn't plan for and a credit score that isn't helping — you've got options. Real ones.

Call: 801-377-3333

Apply online: www.desertrockcapital.com/apply-now/

Walk in: Our Salt Lake City branch is open until 8 PM, Monday through Saturday.

You can also visit our personal loans page to see how signature loans compare to other options, or browse our FAQ for more answers.

A decision usually takes about 30 minutes. And nobody's going to give you that look.